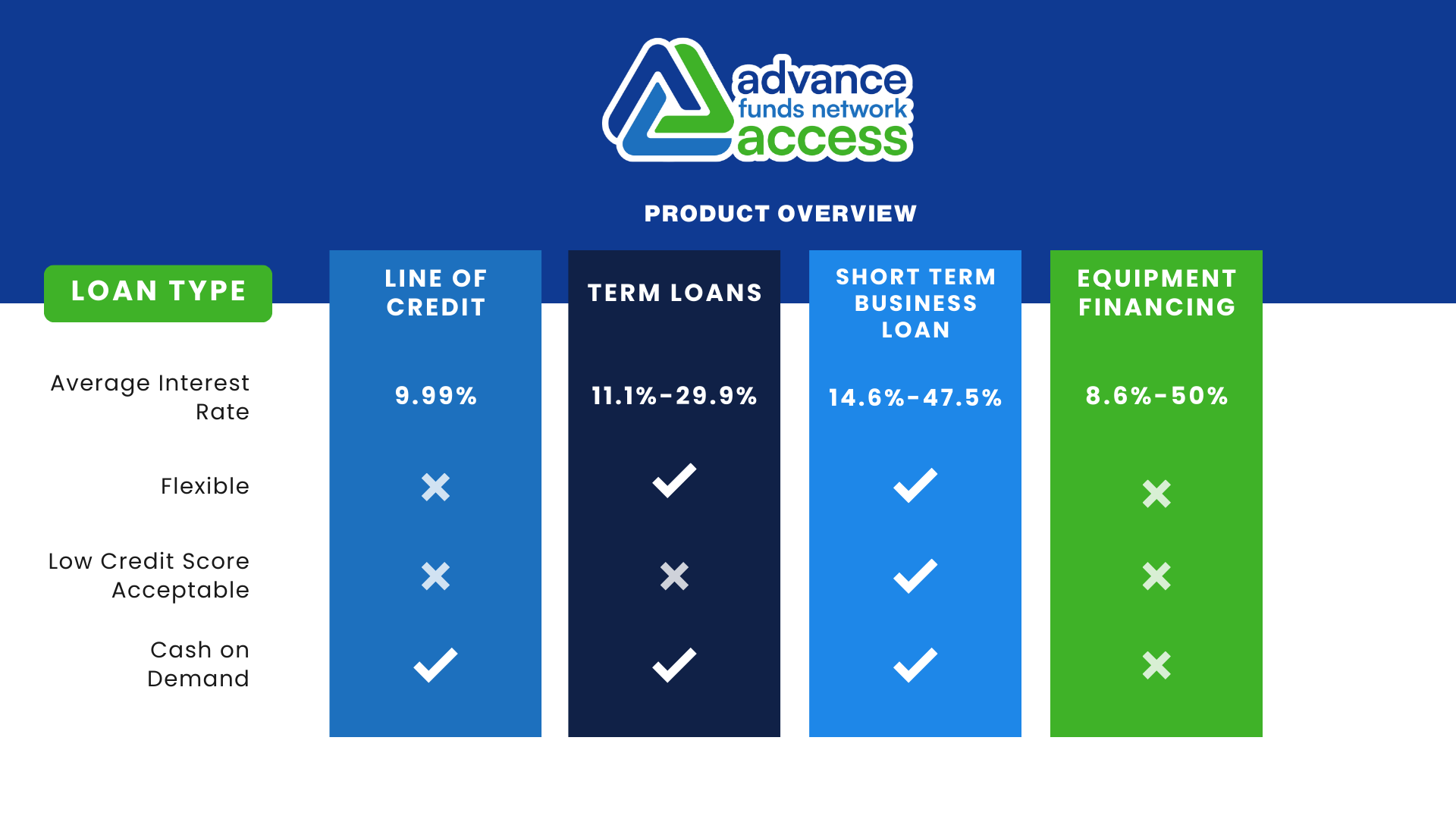

Line of Credit

Term loans provide financing over a specified period, offering lower fixed rates and payments, ensuring consistency throughout the term. Unlike advances, term loans are not upfront payments; instead, they enable businesses to benefit from potential tax write-offs on the interest.

Generally, minimal to no fees are associated with term loans, with transactions in Canada typically processed within 2 to 5 business days. Term lengths range from 6 to 24 months (6 to 18 months in Canada), with fees typically ranging from 0% to 2%.

For approvals exceeding $150,000, tax returns may be requested, while transactions below this threshold may not require such documentation. Various payment structures, including daily, weekly, and biweekly, are available, with monthly options not available in Canada.

Businesses typically occupying first or second positions for repayment priority are favored for term loans. While they can serve as payoff options for existing positions, term loans generally do not accommodate stacking multiple loans. Eligibility criteria often include a monthly revenue of $20,000 or more, a credit score of at least 650, and a minimum of one year in business.

If businesses fail to meet all the following criteria, monthly payment options are not available, reverting to daily or weekly structures: maintaining daily balances of $10,000, possessing a credit score of 650 or higher, operating for at least five years, and avoiding more than six negative days in the past three months.